Two men have been charged by New York prosecutors with stealing secret computer code from a high-frequency trading firm in an effort to start their own business.

Two men have been charged by New York prosecutors with stealing secret computer code from a high-frequency trading firm in an effort to start their own business.

Americans are spending enough to keep the economy rolling, but don’t expect them to splurge unless their paychecks start to grow. Neil Shah reports on the News Hub. Photo: Getty Images.

A year after Hurricane Isaac flooded coastal Louisiana and Mississippi, residents Braithwaite are in limbo. Braithwaite sits outside of the floodwalls built post-Hurricane Katrina, leaving many residents facing prohibitive flood insurance costs. (Aug. 26)

Justin Timberlake wins video of the year, reunites with ‘N Sync at the MTV Video Music Awards, while Miley Cyrus gets provocative and Taylor Swift shows her mean streak. (26 Aug.)

The Post’s David Fahrenthold examines the amount of federal spending, workers, rules and buildings over the years.

Emerging market nations can be adversely affected by large swings in investment, and must therefore develop tools to control credit flows or risk relinquishing any independent monetary policy. That was the finding of a paper presented at the Kansas City Federal Reserve’s monetary policy symposium at Jackson Hole, which highlighted the global impact of the unconventional monetary policy of the United States and other major central banks.

By CountingPips.com

Weekly CFTC Net Speculator Report

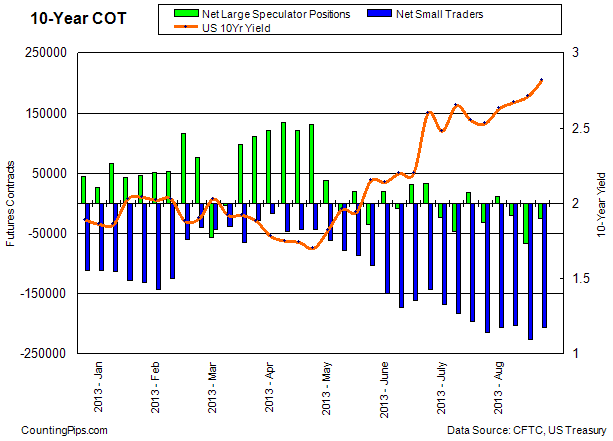

10 Year Treasuries: Large trader and speculators reduced their bearish positions last week for 10-year treasury notes in the futures markets after pushing 10-year notes to their most bearish position of 2013 the previous week. 10-year treasury non-commercial contracts totaled a net position of -24,840 contracts in the data reported for August 20th. This is an improvement of +41,592 contracts from the previous week’s total of -66,432 net contracts on August 13th. In the same time-frame, the yield on the 10 Year treasury note rose from 2.71 on Tuesday August 13th to 2.82 on Tuesday August 20th, according to US Treasury data.

Last 6 Weeks of Large Trader Positions

| Date | Net Large Specs | Weekly Change | 10 Year Yield |

| 07/16/2013 | 17735 | 64845 | 2.55 |

| 07/23/2013 | -32312 | -50047 | 2.53 |

| 07/30/2013 | 11903 | 44215 | 2.63 |

| 08/06/2013 | -20096 | -31999 | 2.67 |

| 08/13/2013 | -66432 | -46336 | 2.71 |

| 08/20/2013 | -24840 | 41592 | 2.82 |

*COT explanation: The weekly cot report summarizes the total trader positions for open contracts in the futures trading markets. The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

Article by CountingPips.com – Forex News & Market Analysis

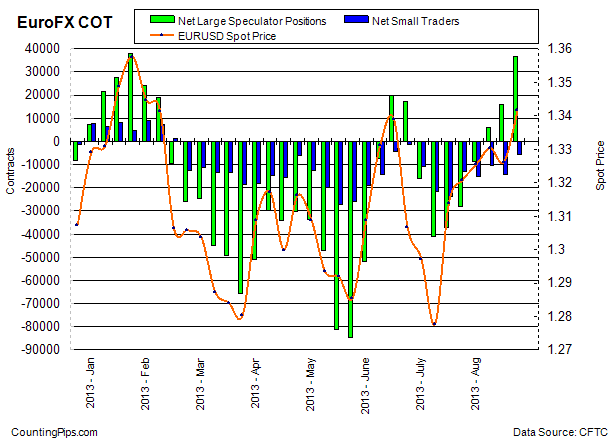

The weekly Commitments of Traders (COT) report, released on Friday by the Commodity Futures Trading Commission (CFTC), showed that large futures traders and currency speculators continued to cut back on their bullish bets of the US dollar last week for a fifth consecutive week.

Non-commercial large futures traders, including hedge funds and large International Monetary Market speculators, decreased their overall US dollar long positions to a total of $13.54 billion as of Tuesday August 20th. This was a decrease of $4.08 billion from the total long position of $17.62 billion that was registered on August 13th, according to calculations by Reuters that calculates this amount by the total of US dollar contracts against the combined contracts of the euro, British pound, Japanese yen, Australian dollar, Canadian dollar and the Swiss franc.

US dollar overall long positions remained at the lowest level since June 25th when long bets equaled $13.28 billion.

COT explanation: The weekly cot report summarizes the total trader positions for open contracts in the futures trading markets. The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and non-reportable traders (usually small traders/speculators).

Individual Currencies Large Speculators Positions in Futures:

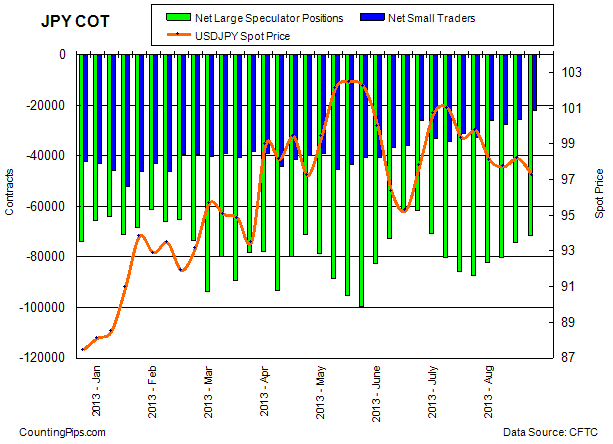

The large non-commercial net positions for each of the individual major currencies directly against the US dollar last week saw weekly increases for the euro, British pound sterling, Japanese yen and the New Zealand dollar while the Swiss franc, Canadian dollar, Australian dollar and the Mexican peso had declining numbers of large speculator positions for the week.

Notable changes:

Euro net speculative contracts improved for the sixth straight week and are at their 2nd best level of 2013 and highest level since February 5th when bullish positions totaled +37,952 contracts.

Individual Currency Charts:

EuroFX:

Last Six Weeks of Large Trader Positions: EuroFX

| Date | Large Trader Net Positions | Weekly Change |

| 07/16/2013 | -37165 | 3735 |

| 07/23/2013 | -27900 | 9265 |

| 07/30/2013 | -8504 | 19396 |

| 08/06/2013 | 6061 | 14565 |

| 08/13/2013 | 16057 | 9996 |

| 08/20/2013 | 36746 | 20689 |

British Pound Sterling:

Last Six Weeks of Large Trader Positions: Pound Sterling

| Date | Lg Trader Net | Weekly Change |

| 07/16/2013 | -37446 | -3187 |

| 07/23/2013 | -49653 | -12207 |

| 07/30/2013 | -49463 | 190 |

| 08/06/2013 | -46033 | 3430 |

| 08/13/2013 | -46521 | -488 |

| 08/20/2013 | -39522 | 6999 |

Japanese Yen:

Last Six Weeks of Large Trader Positions: Yen

| Date | Lg Trader Net | Weekly Change |

| 07/16/2013 | -85762 | -5457 |

| 07/23/2013 | -87496 | -1734 |

| 07/30/2013 | -82135 | 5361 |

| 08/06/2013 | -80213 | 1922 |

| 08/13/2013 | -74462 | 5751 |

| 08/20/2013 | -71721 | 2741 |

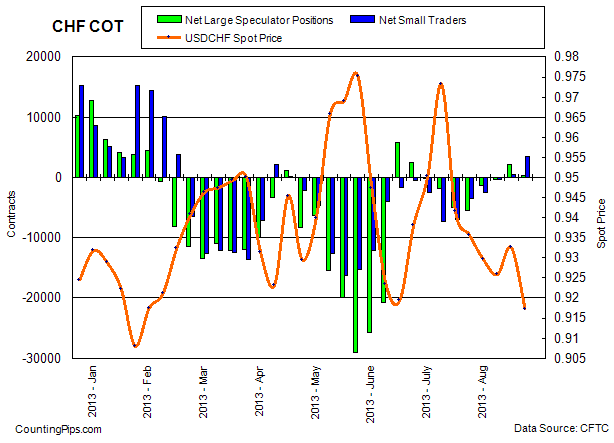

Swiss Franc:

Last Six Weeks of Large Trader Positions: Franc

| Date | Lg Trader Net | Weekly Change |

| 07/16/2013 | -4969 | -3193 |

| 07/23/2013 | -5433 | -464 |

| 07/30/2013 | -1261 | 4172 |

| 08/06/2013 | -325 | 936 |

| 08/13/2013 | 2136 | 2461 |

| 08/20/2013 | 291 | -1845 |

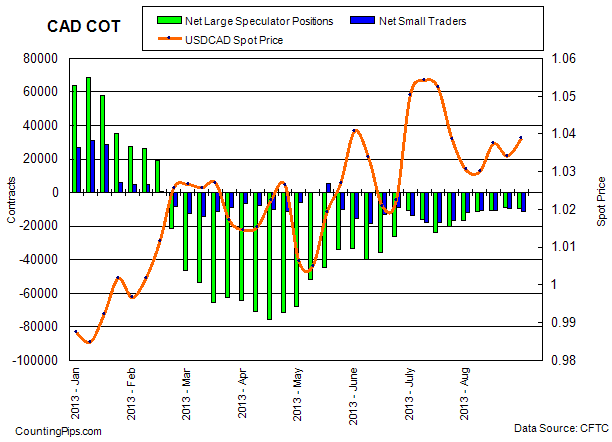

Canadian Dollar:

Last Six Weeks of Large Trader Positions: CAD

| Date | Lg Trader Net | Weekly Change |

| 07/16/2013 | -20043 | 3786 |

| 07/23/2013 | -16758 | 3285 |

| 07/30/2013 | -11434 | 5324 |

| 08/06/2013 | -10436 | 998 |

| 08/13/2013 | -9081 | 1355 |

| 08/20/2013 | -9544 | -463 |

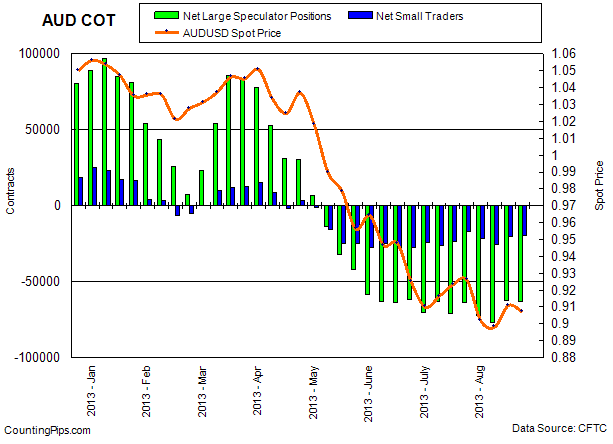

Australian Dollar:

Last Six Weeks of Large Trader Positions: AUD

| Date | Lg Trader Net | Weekly Change |

| 07/16/2013 | -70686 | -7431 |

| 07/23/2013 | -63982 | 6704 |

| 07/30/2013 | -72573 | -8591 |

| 08/06/2013 | -76779 | -4206 |

| 08/13/2013 | -62721 | 14058 |

| 08/20/2013 | -63183 | -462 |

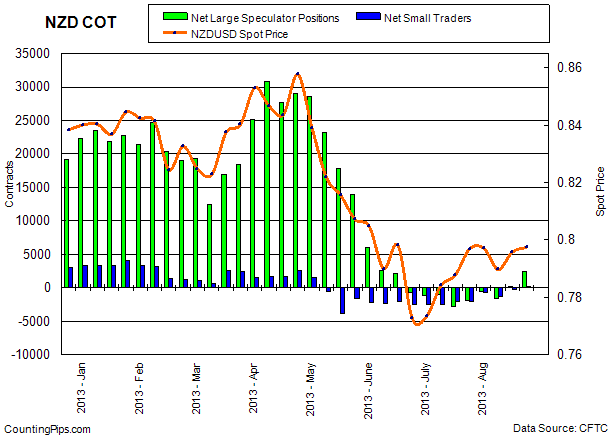

New Zealand Dollar:

Last Six Weeks of Large Trader Positions: NZD

| Date | Lg Trader Net | Weekly Change |

| 07/16/2013 | -2744 | -1736 |

| 07/23/2013 | -1846 | 898 |

| 07/30/2013 | -520 | 1326 |

| 08/06/2013 | -1539 | -1019 |

| 08/13/2013 | 197 | 1736 |

| 08/20/2013 | 2390 | 2193 |

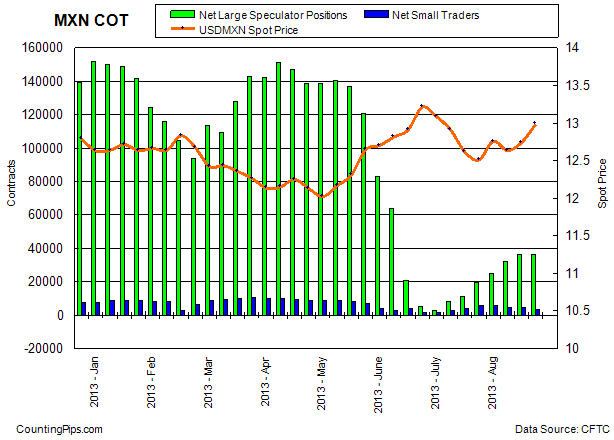

Mexican Peso:

Last Six Weeks of Large Trader Positions: MXN

| Date | Lg Trader Net | Weekly Change |

| 07/16/2013 | 11366 | 3331 |

| 07/23/2013 | 19799 | 8433 |

| 07/30/2013 | 24888 | 5089 |

| 08/06/2013 | 32125 | 7237 |

| 08/13/2013 | 36320 | 4195 |

| 08/20/2013 | 36131 | -189 |

The Commitment of Traders report is published every Friday by the Commodity Futures Trading Commission (CFTC) and shows futures positions data that was reported as of the previous Tuesday (3 days behind).

Each currency contract is a quote for that currency directly against the U.S. dollar, a net short amount of contracts means that more speculators are betting that currency to fall against the dollar and a net long position expect that currency to rise versus the dollar.

(The graphs overlay the forex spot closing price of each Tuesday when COT trader positions are reported for each corresponding spot currency pair.)

See more information and explanation on the weekly COT report from the CFTC website.

Article by CountingPips.com

A big jump in Microsoft helped lift the Dow Jones industrial average

As questions swirl around Nasdaq’s latest glitch, one issue that is central to the discussion is the role of high speed trading in today’s market. Charles Jones, finance professor at Columbia Business School, joins MoneyBeat. Photo: Getty Images.