By The Life Science Report – Source: Peter Epstein for Streetwise Reports 07/17/2020

In the time of Covid-19, Peter Epstein of Epstein Research breaks down the investment opportunity offered by CloudMD.

Please note: News came out July 16, the day this article was written, on CloudMD, the subject of this article. The news is not addressed in this article, but is considered to be good news and will be discussed in a future write-up.

Gold is at a nine-year high. Dozens of gold juniors have seen their share prices soar this year. Investors see the writing on the wall; gold fundamentals are incredibly strong due to Covid-19-induced government debt issuance, money printing and deficit spending, with no end in sight.

Once people realize a paradigm shift is at hand, they’re not afraid to buy smaller, riskier companies, seeking large gains. Covid-19 is ushering in a number of paradigm shifts, but few as clear-cut as gold.

Readers beware, some trends have already been exploited. Online shopping? Amazon is up 92% since March. Teleconferencing? Zoom up 140%. Online education? K-12 Inc., +175%. Movie streaming? Netflix, +110%.

Free Reports:

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get Our Free Metatrader 4 Indicators - Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Telemedicine is hot and will remain strong for years, not months or weeks

Like gold, I think telemedicine’s time has come. Covid-19 has vaulted this niche industry into the big leagues in a matter of months rather than years. Regulators were forced to rapidly understand and get behind tele-sessions. Insurance companies have had to do the same. Truly a win-win-win for patients, doctors/nurses and medical practices.

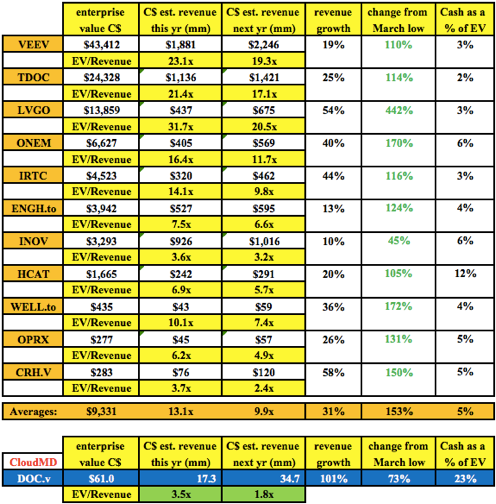

If one agrees that telemedicine is a bona fide paradigm shift in healthcare services, then one should consider investing in smaller companies with potentially more upside (albeit with commensurately more risk) than firms like $50 billion ($50B) Veeva Systems (VEEV:NYSE), which is +104% since March; $24B Teladoc Health Inc. (TDOC:NYSE), +114%, or $14B Livongo Health (LVGO:NASDAQ), +430%!

Much of telemedicine is new, everyone is learning as they go. Successes will be handsomely rewarded. Well-funded, small, smart, fast, nimble companies probably have a two- or three-year window to get it right. The top companies will get taken out at attractive valuations.

CloudMD well positioned to thrive in telemedicine, then get acquired

A company that’s ideally positioned to rapidly expand in telemedicine and potentially be acquired is CloudMD Software & Services Inc. (DOC:TSX.V; DOCRF:OTCQB; 6PH:FSE). It has a market cap of $72.7 million ($72.7M) and an Enterprise Value (EV) {market cap + debt cash} of ~$61M. Revenue is growing very rapidly, potentially increasing by >400% from $6.8M in 2019 to the consensus estimate of $34.7M in 2021.

CloudMD is revolutionizing the delivery of healthcare by providing patients easy, fast access to all aspects of their care via phone, tablet, laptop or desktop computer. The company offers SAAS (software as a service) based solutions to medical clinics across Canada. That’s on top of owning and operating brick-and-mortar clinics and acquiring new facilities.

Management has developed or acquired proprietary technology that delivers high-quality care through connected primary care clinics, telemedicine and artificial intelligence. CloudMD currently provides service to an ecosystem of 376 clinics in eight provinces, over 3,000 licensed practitioners, with access to nearly 3 million patient charts.

Hybrid business model; clinics + telemedicine + SAAS-like margin potential

Following the SAAS business model, CloudMD has the potential to be a high-margin, stable (low churn), rapidly growing company, with long-lasting (recurring) revenue. As shown in the chart below, the company has the fastest [expected] revenue growth (2021 over 2020) at 101% versus an average of 31%. Part of the reason is that revenue is launching off of a small base, but the company also compares favorably on its EV/revenue multiple (3.5x/1.8x) versus averages of (13.1x/9.9x). So, fastest-growing, cheapest valuation.

Management is prudently pursing a hybrid approach to healthcare delivery in Canada. In addition to telemedicine the team continues to acquire, own and optimize conventional clinics. I believe this approach captures the most efficient and cost-effective way to gain market share. There’s a finite number of doctors, nurses and family offices. Rolling them up into CloudMD, before they join other companies, is a winning strategy.

Medium-sized companies can only grow so fast organically. They need to acquire growth in order to make themselves attractive to larger players. There are a lot of small-cap telemedicine ventures, but only a few are high quality, with visionary management teams, strong balance sheets and rapid revenue growth. Fewer still offer compelling valuations.

After raising $15M last month, management has amassed a sizable war chest with which to make accretive acquisitions. CloudMD is making acquisitions of businesses at under 1x revenue, integrating and streamlining them, making the revenue worth more.

Larger players pay higher revenue multiples, M&A critically important

Larger entities can afford to pay well above 1x revenue because they unleash even greater synergies and economies of scale, and gain the opportunity to cross-sell new services. It appears that management has the financial wherewithal to acquire about $30M in annual revenue. That’s 86.5% of the consensus estimate for 2021 of $34.7M.

Once companies like CloudMD gain reasonable scale, they become prime takeover targets themselves. To be clear, this chain of events only works while the underlying sector is strong. Telemedicine is strong!

The company’s shares have languished; some fear an upcoming selloff as two blocks totaling ~6M shares (private placements at $0.48; current share price $0.64) become free-trading on July 20 and 30. Some of the feared selling has probably already taken place. Over the past three months, average daily trading volume was 1.3M shares (per Stockwatch).

As the telemedicine sector soared from late March on, CloudMD shares initially participated, rising from $0.37 to $0.95. However, the stock has settled back to $0.64. Early last month, the company issued $15M worth of shares at $0.70, with a half-warrant at $1.00, giving them the largest cash holdings relative to EV (23%) of any peer I could find.

CloudMD and its CEO are not new to telemedicine; this is a people business

CloudMD has been actively involved in the healthcare space for years. In May 2018, it acquired HealthVue Ventures, a family practice with three clinics performing telemedicine, and other more routine services. It’s been over two years that management has seen virtual meetings as the wave of the future. CEO Dr. Hamza has been practicing telemedicine for seven years, making him a leading expert in this nascent field.

Patients can avoid missing work or school by using virtual meetings, negating the need for childcareor worse, having to drag children to the doctor’s office. For some, getting to an appointment on time, and also planning the rest of the day’s activities, can be difficult and stressful.

Evidence from four months of pandemic in North America, as telemedicine has been thrust upon us, suggests most patients find it to be as good, or better, than in-person visits. Going to the doctor takes time and logistical preparation and carries added expenses. By car or public transport, finding/paying for parking, paying and waiting for Uber rides, or getting rides from friends and family. A half-hour appointment can turn into a much longer, unpredictable, stress-provoking ordeal.

In addition to being much more convenient, patients are reporting more time with doctors and feeling that they have a doctor’s full attention. Incremental, high-quality time spent with doctors and nurses means more questions asked and answered. In-person visits will still be needed, but the mix is shifting in favor of virtual consultations.

Patients like telemedicine; everyone benefits from less exposure to germs

As patients get used to the ease of telemedicine, pundits believe they will initiate more sessions with doctors than they otherwise would have. Also, patients who rarely, if ever, seek medical advice or treatmentdue to a fear of doctors, hospitals, germs or social anxietymight find telemedicine appealing.

From the doctor’s point of view, they can expect to “see” more patients per week, or the same number in fewer days (five days’ worth of patients in four days = Fridays off). Patients are less likely to cancel or not show up to appointments. If a doctor is away on business, at a conference, she/he could still meet remotely.

Earlier this week, the CDC director predicted that this fall and winter will be “one of the most difficult times we’ve experienced in American public health.” No one wants to hear thatI sincerely hope he’s wrongbut it means that investors will be thinking about and experiencing telemedicine for quite some time.

Doctors like telemedicine; everyone benefits from less exposure to germs

Healthcare is one of the toughest businesses to operate and especially hard to enter. It takes years of experience and, importantly, trusted relationships and teamwork. New companies can’t obtain credibility overnight. Yet credibility is critical to attracting new patients, doctors, nurses and family offices to join small companies like CloudMD.

Joining a smaller group of highly talented professionals has advantages over being a tiny fish in a giant pond. New executives and business partners can make a meaningful difference in how CloudMD evolves. In the end, telemedicine is only as good as the people/groups behind it. That’s where the story gets really exciting and where the company can deliver tremendous shareholder value.

Attracting healthcare rock stars, in part by offering sign-on bonuses, equity stakes, autonomy, a chance to help build a fantastic company, flexible hours/places to work (home, travel, holiday or in a medical office)getting this right will make an investment in CloudMD really pay off! Great people attract great people. Great people have large networks. Give them CA$15M to deploy? Great things should follow.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Sign up for our FREE newsletter at: www.streetwisereports.com/get-news

Peter Epstein’s Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about CloudMD Software and Services, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of CloudMD are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, CloudMD was an advertiser on [ER]. Peter Epstein owned no shares, options or warrants in the company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts and financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events and news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure:

1) Peter Epstein’s disclosures are listed above.

2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with CloudMD. Please click here for more information. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of CloudMD, a company mentioned in this article.

6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

( Companies Mentioned: DOC:TSX.V; DOCRF:OTCQB; 6PH:FSE,

)

![]()