Great Recession? What Great Recession?

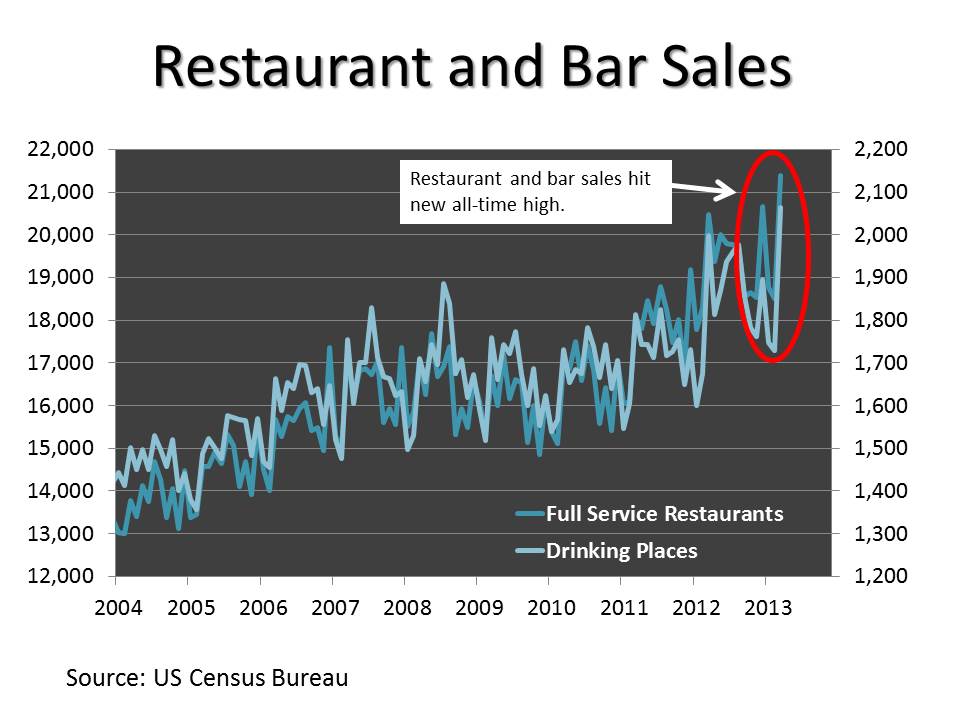

After flatlining for five years, restaurant and bar sales hit new all-time highs earlier this month (see chart). It would seem that the scrimping and ramen noodle eating that became so common after the 2008 meltdown is now a distant memory.

Well, sort of. There are a couple things to keep in mind. To start, the sales data do not take into account inflation, which, while modest, makes the recent gains a little less spectacular than they look. And Americans haven’t exactly returned to their free spending ways; according to the National Restaurant Association, 49 percent of American adults do not eat in restaurants as often as they would like.

There is also a demographic angle at work. 20-somethings are splurging more on meals and booze, but nearly half of the 50-64 age bracket—which roughly corresponds to America’s Baby Boomers—are spending less and consider the lower spending to be their “new normal.”

For anyone with an academic interest in demographics (yes, there are some of us who do), this is precisely what you would expect. The Baby Boomers are saving for a retirement that most are not prepared for. And even under more normal economic conditions, spending on food and alcohol in restaurants and bars tends to peak in the mid-50s. I appears that, once the kids leave the nest, Americans like to enjoy one last hurrah of feasting and boozing before they settle down.

Meanwhile, while unemployment is still high among the young, most are employed and earning more than at any time in their lives. Most 20-somethings are also childless, meaning that a larger percentage of their incomes are disposable.

And importantly, this large generation—alternatively called Gen Y, the Echo Boomers, or the Millennials—has a lot of spending left to do. The largest cohort is still in their early 20s.

So, with all of this said, how do we profit?

I’ve been a fan of alcoholic beverage stocks for years, and Heineken ($HEINY) and Diageo ($DEO) are both long-time portfolio holdings. But these are primarily “emerging market lite” plays, as both have better prospects in the developing world than in North America.

What about restaurant stocks?

I’ve had several restaurant and casual dining stocks on my watch list with the Echo Boomers in mind. The problem is that while I might loves some of the companies, I’m not too fond of the stocks.

Consider Chipotle Mexican Grill ($CMG). It’s a compelling story backed by strong, secular trends: the move towards healthier and more organic eating and the convergence between fast food and casual dining. And frankly, I could eat there every day and never get tired of it.

There is one big problem: while Chipotle’s burritos are reasonably priced, its stock isn’t. It currently trades for nearly 30 times expected earnings and 4 times sales.

Buffalo Wild Wings Inc. ($BWLD), another trendy casual dining stock, is likewise a little too pricey for my liking. It trades for over 20 times expected earnings. Panera ($PNRA) isn’t any cheaper. It trades for 24 times expected earnings. None of these three pay a dividend.

Moving up the price ladder, we get to Darden Restaurants ($DRI), the owner of the Olive Garden, Red Lobster, and Longhorn Steakhouse among others and Brinker International ($EAT), the owner of Chili’s and Maggiano’ Little Italy. Brinker has had a decent run, up about 60% over the past two years, compared to around 20% for the S&P 500. Darden has lagged and is flat for the period.

Brinker and Darden are not sexy. They epitomize the American suburbs, which is about as anti-sexy as you can get when it comes to a night out. These restaurants are also the restaurants frequented by the Baby Boomers when they were raising their kids. Those same Boomers are now past that stage, and their children are not yet in it themselves.

So, we can’t expect a huge surge in revenues tomorrow. However, with the American housing market recovering and with the Echo Boomers reaching the marriage and family formation stages of their lives, there is a long-term, 10-15-year story here.

Brinker is not particularly overpriced at 14 times expected earnings and pays a 2% dividend. But Darden would seem to be the more attractive of the two. It’s slightly more expensive at 16 times earnings, but it pays a nice 3.7% dividend. Importantly, the company has been growing that dividend aggressively since 2008.

Darden isn’t a homerun stock, but it should be a nice income producer with the potential for decent growth in the years ahead as the Echo Boomers settle down and move to the ‘burbs.

Sizemore Capital is long HEINY and DEO. This article first appeared on InvestorPlace.