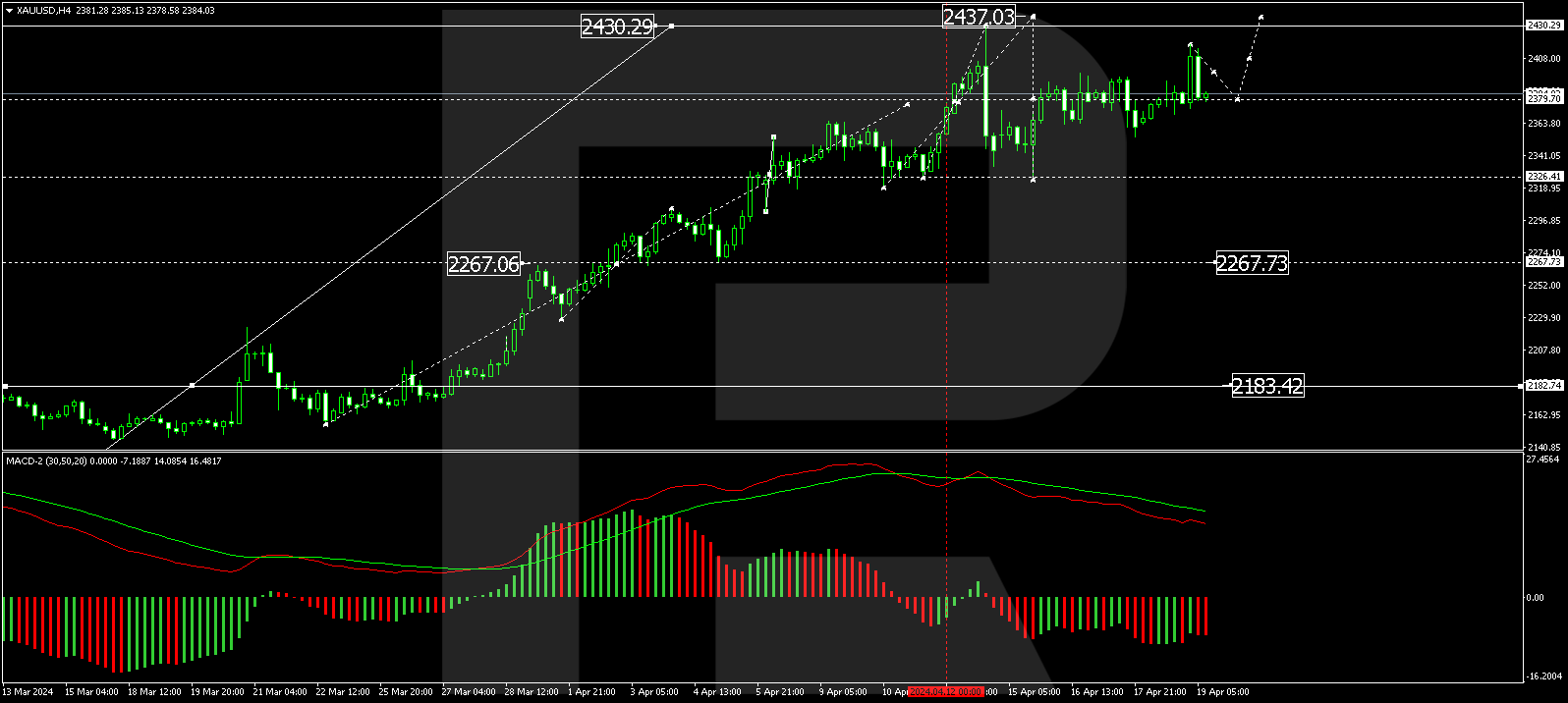

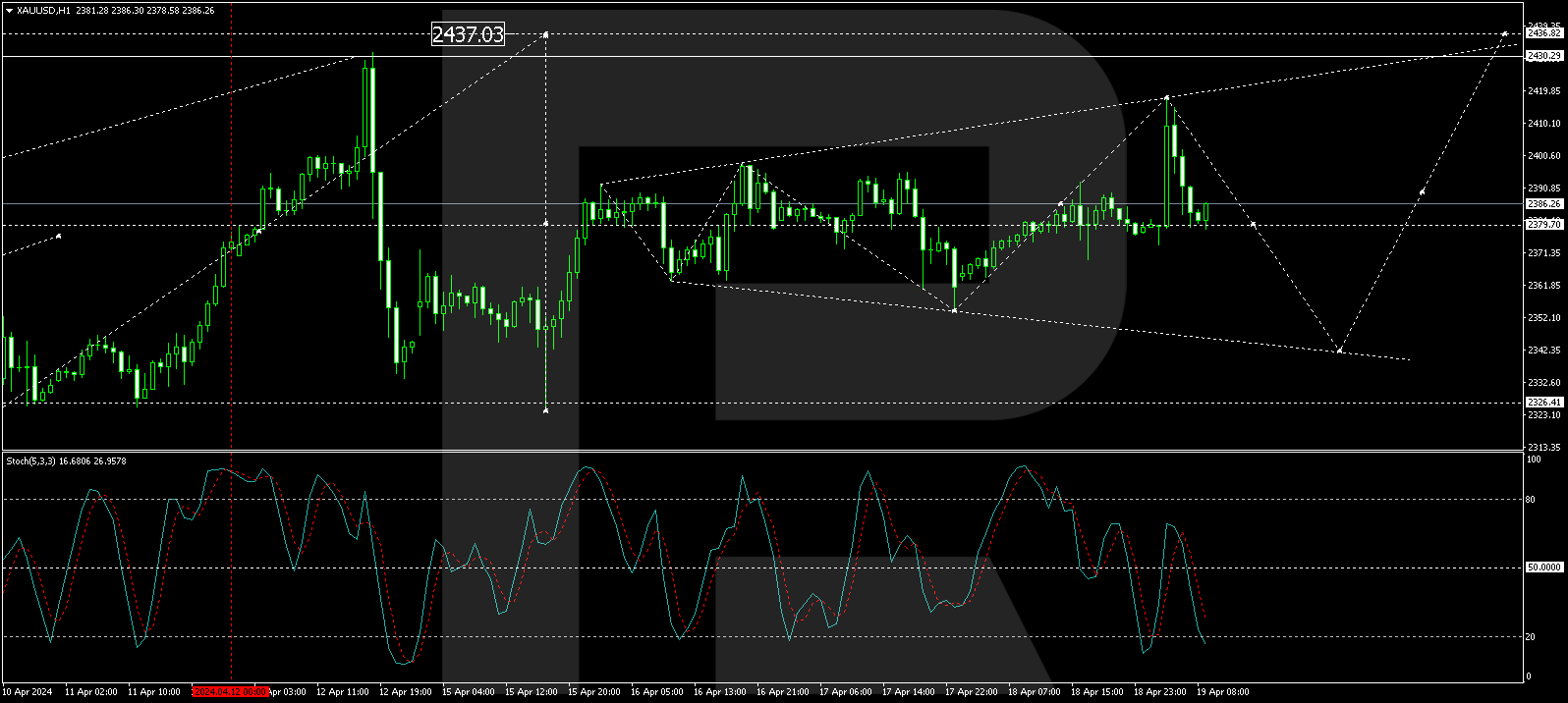

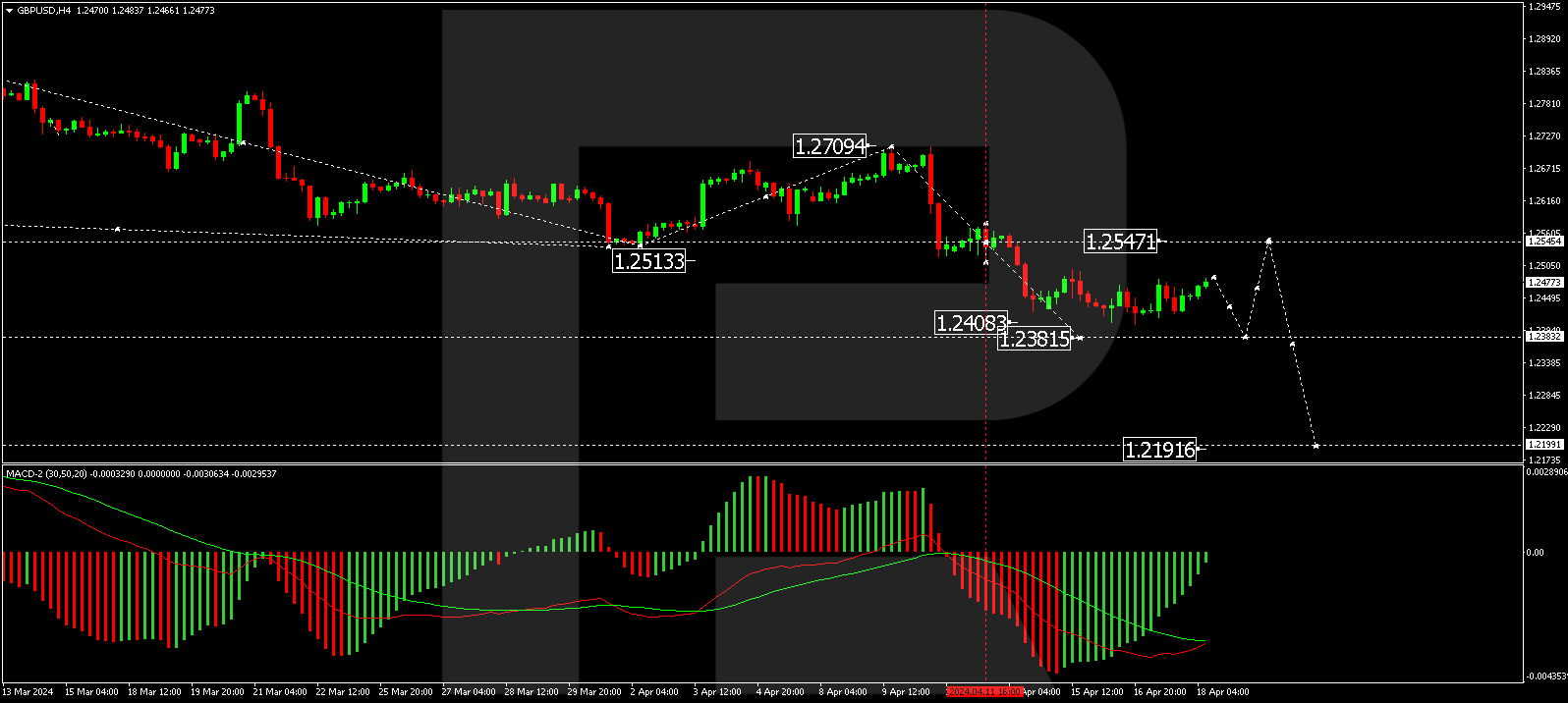

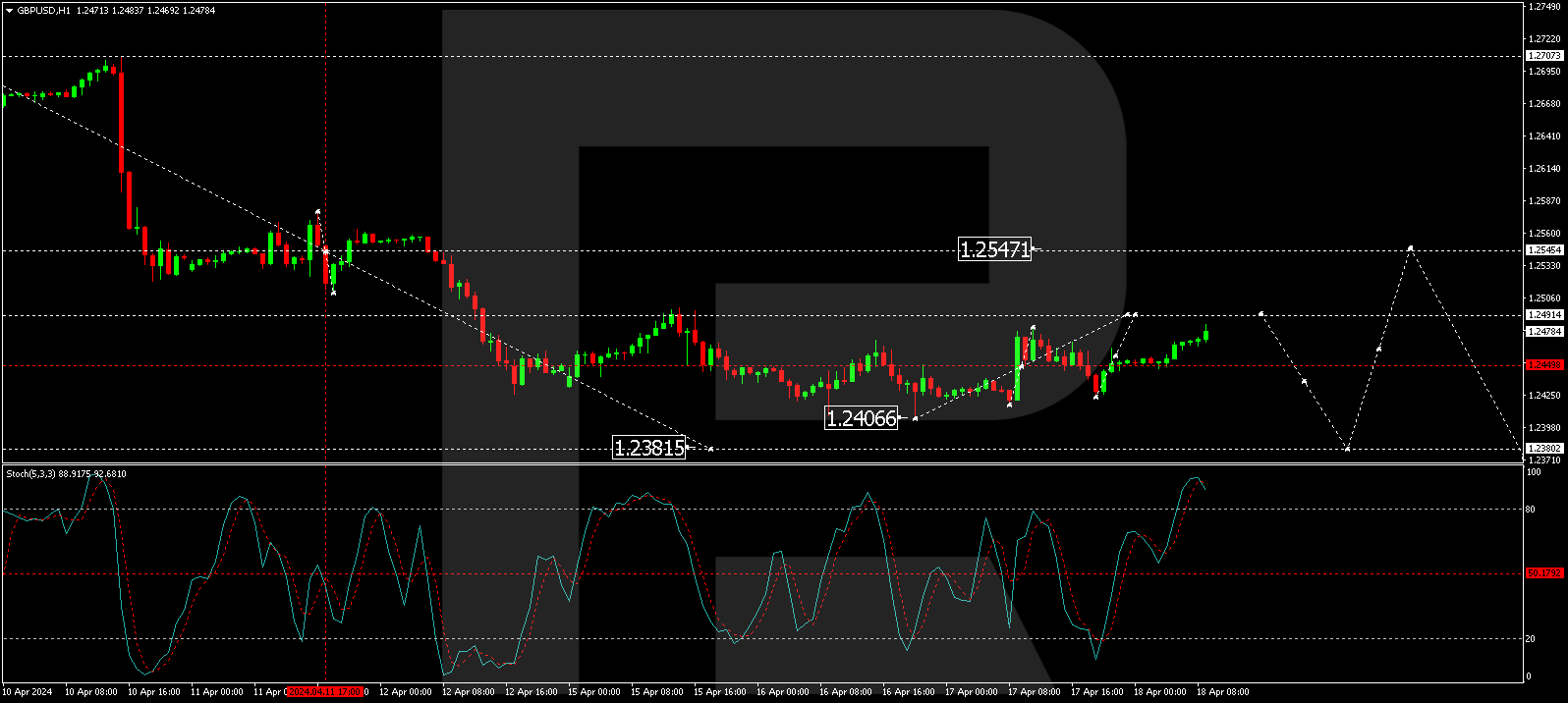

By JustMarkets

At Monday’s close, the Dow Jones (US30) Index decreased by 0.65%, while the S&P 500 (US500) Index was down 1.20%. The NASDAQ Technology Index (US100) closed yesterday negative at 1.79%. The US dollar initially declined on Monday amid lower liquidity demand, as stocks rose after geopolitical concerns eased amid hopes that diplomatic efforts would curb the conflict between Iran and Israel. However, the US dollar jumped sharply in the US session after March, and US retail sales rose more than expected, a hawkish factor for Fed policy. In addition, the inability of equities to hold on to the early rally caused additional liquidity demand for the dollar. That said, last night, Israel’s defense minister said that Israel has no choice but to retaliate against Iran for its drone missile attack on Israel over the weekend.

Salesforce (CRM) shares fell more than 7%. They topped the list of losers in the S&P 500 and Dow Jones Industrials following a Bloomberg report that the company is interested in acquiring Informatica, which analysts say could attract regulatory attention. Atlassian (TEAM) slid more than 7% and topped the list of losers in the Nasdaq 100 after Mizuho Securities cut its price target on the company’s shares to $240 from $265. Tesla (TSLA) closed down more than 5%, topping the Nasdaq 100 losers list, after CEO Musk said the company will cut its global workforce by more than 10% as demand for electric vehicles slows.

Equity markets in Europe mostly went up yesterday. Germany’s DAX (DE40) rose by 0.54% (up -1.28% on the week), France’s CAC 40 (FR40) closed higher by 0.43%, Spain’s IBEX 35 (ES35) closed at its opening price, and the UK’s FTSE 100 (UK100) closed negative 0.38% on Monday. European stock markets opened lower on Tuesday as strong US retail sales data reinforced expectations that the Federal Reserve will postpone interest rate cuts. Investors are also keeping a close eye on developments in the Middle East amid concerns that an Iranian attack on Israel over the weekend could lead to a wider conflict in the region.

The latest data showed an unexpected increase in the UK unemployment rate to 4.2%, exceeding expectations of 4.0%, while wage growth slowed gradually. Traders adjusted their forecasts for the Bank of England and the Federal Reserve to cut interest rates this year, driven by strong US inflation figures. The Bank of England rate is expected to fall to 4.75% by the end of 2024 from the current 5.25%, a significant change from the previous forecast that suggested a rate cut to 4.5% by December.

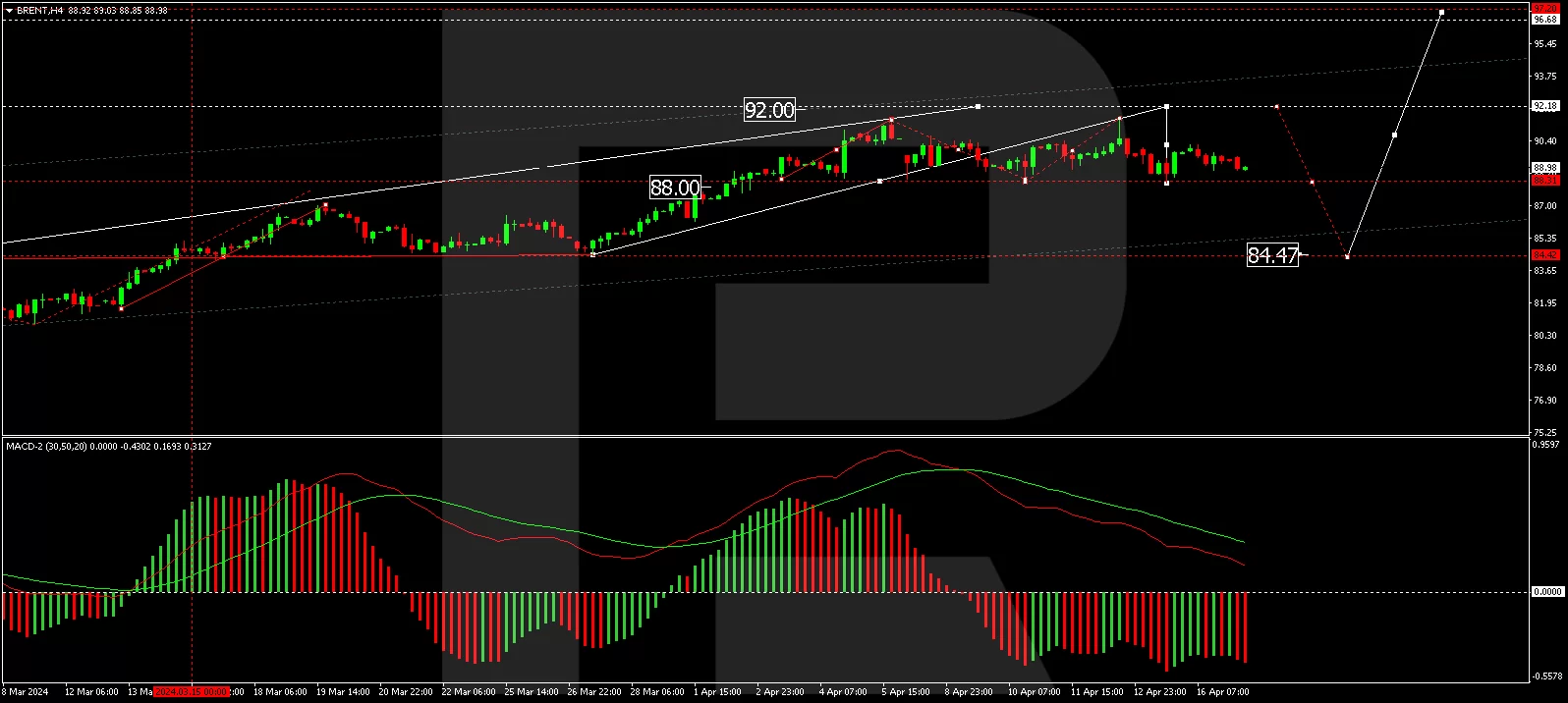

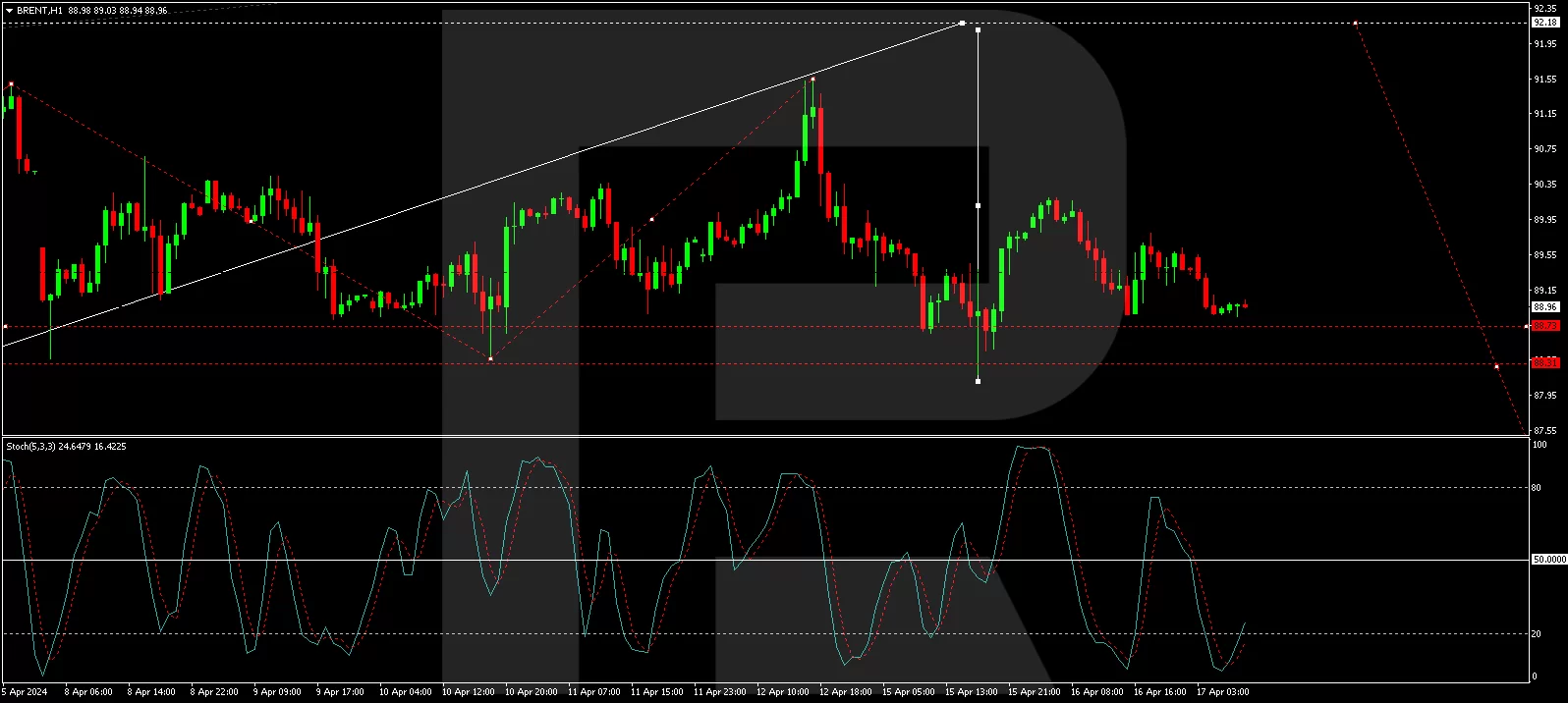

WTI crude oil prices rose to around $86 a barrel on Tuesday, reversing losses from the previous session as investors await Israel’s response. Israel’s military chief said his country would respond to the attack, with reports suggesting they were targeting key targets in Iran. Iran is a leading OPEC member, producing more than 3 million barrels of crude oil daily.

Asian markets were predominantly down. Japan’s Nikkei 225 (JP225) was down 0.65% yesterday, China’s FTSE China A50 (CHA50) was up 2.7%, Hong Kong’s Hang Seng (HK50) lost 0.99% yesterday, and Australia’s ASX 200 (AU200) was negative 0.75%.

Asian stocks fell sharply on Tuesday, following an overnight decline on Wall Street amid lingering concerns over geopolitical tensions in the Middle East and a longer-term interest rate hike in the US. However, losses in Chinese stocks were slightly less than their peers as gross domestic product (GDP) data showed the country’s economy grew more than expected in the first quarter. China’s economy grew 5.3% y/y in the first quarter of 2024, exceeding market forecasts of 5.0% and following 5.2% growth in the previous period. This was the sharpest annual growth since Q2 2023, helped by continued supportive measures from Beijing, while the Lunar New Year festival also boosted consumer spending. Fixed asset investment rose by 4.5% in the first three months of the year, the highest in three years and above the consensus forecast of 4.3%. Meanwhile, March data showed that industrial production and retail sales rose less than expected, underscoring the need for further policy easing for the economy. At the same time, the unemployment rate came in at 5.2% in March, remaining near February’s 7-month high of 5.3%.

S&P 500 (US500) 5,061.82 −61.59 (−1.20%)

Dow Jones (US30) 37,735.11 −248.13 (−0.65%)

DAX (DE40) 18,026.58 +96.26 (+0.54%)

FTSE 100 (UK100) 7,965.53 −30.05 (−0.38%)

USD Index 106.35 +0.14 (+0.13%)

Important events today:

- – China GDP (q/q) at 05:00 (GMT+3);

- – China Industrial Production (y/y) at 05:00 (GMT+3);

- – China Unemployment Rate (m/m) at 05:00 (GMT+3);

- – China Retail Sales (m/m) at 05:00 (GMT+3);

- – UK Average Earnings Index (m/m) at 09:00 (GMT+3);

- – UK Claimant Count Change (m/m) at 09:00 (GMT+3);

- – UK Unemployment Rate (m/m) at 09:00 (GMT+3);

- – German ZEW Economic Sentiment (m/m) at 12:00 (GMT+3);

- – Eurozone ZEW Economic Sentiment (m/m) at 12:00 (GMT+3);

- – Eurozone Trade Balance (m/m) at 12:00 (GMT+3);

- – Canada Consumer Price Index (m/m) at 15:30 (GMT+3);

- – US Building Permits (m/m) at 15:30 (GMT+3);

- – US Industrial Production (m/m) at 16:15 (GMT+3);

- – UK BoE Gov Bailey Speaks at 20:00 (GMT+3);

- – Canada BoC Gov Macklem Speaks at 20:15 (GMT+3);

- – US Fed Chair Powell Speaks at 20:15 (GMT+3).

By JustMarkets

This article reflects a personal opinion and should not be interpreted as an investment advice, and/or offer, and/or a persistent request for carrying out financial transactions, and/or a guarantee, and/or a forecast of future events.