By Lukman Otunuga Research Analyst, ForexTime

The next few days promise to be intense and volatile thanks to key economic data from major economies, updated company earnings and speeches from numerous Federal Reserve officials including Jerome Powell.

Asian stocks were green on Tuesday morning after Wall Street’s main indices closed at record highs overnight. The risk-on sentiment across Asian markets was also helped by strong trade data from China which soothed concerns over slowing growth in the world’s second largest economy.

This positive vibe could seep into European shares before earnings kick off later in the day with JPMorgan and Goldman Sachs reporting their numbers. Investors will also be dished a serving of US inflation data this afternoon which could offer clues over the Federal Reserve’s timeline for easing its bond purchases.

On top of this, the market mood is likely to be influenced by growing concerns over the Delta coronavirus variant negatively impacting the global economic recovery. With so much going on across board with various themes and developments, this could be a week to remember.

Dollar holds its breath ahead of CPI data

Free Reports:

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

The dollar seems to be struggling for direction on Tuesday morning ahead of the US inflation data for June.

Headline CPI is expected to print at 4.9% year-over-year while core CPI is forecast to come in at 4.0%. The monthly reading is expected to drop to 0.5% in June from the 0.6% witnessed in May while core CPI is projected to print 0.4%, down from 0.7% in the previous month. An upside surprise to the inflation data may inject dollar bulls with fresh inspiration as expectations mount over the Federal Reserve tapering asset purchases sooner than expected. However, if the data fails to meet expectations, it could reduce the pressure on the Fed to make a move, resulting in a weaker dollar.

There are a couple of Fed members set to speak later in the day which could add some more spice to the forex markets. Atlanta Fed President Raphael Bostic, Fed President Neel Kashkari and Boston Fed President Eric Rosengren will be under the spotlight today.

Taking a quick look at the technical picture, the Dollar Index (DXY) has found itself in a range with support at 92.00 and resistance at 92.75. A solid break below 92.00 may open the doors towards 91.50. Alternatively, should 92.00 prove to be reliable support, a rebound back towards 92.75 and potentially beyond could be on the cards.

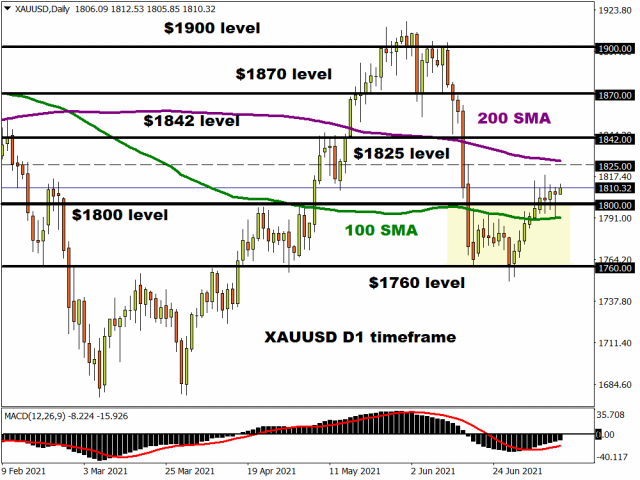

Commodity spotlight – Gold

How gold performs this week may be heavily influenced by the pending US inflation data and Fed Chair Jerome Powell’s testimony later in the week. The precious metal remains sensitive to inflation expectations and speeches from Fed officials, so the next few days could be volatile. In the meantime, gold continues to draw support from global growth concerns and fears over the Covid-19 variants.

Despite the weekly close above $1800, bulls are certainly not out of the woods yet. Gold bugs may face resistance around $1825 as this is where 200-day SMA resides. However, if this zone can be overcome, the next key levels of interest can be found at $1842, $1870 and $1900. Alternatively, a breakdown below $1800 could signal a decline back towards $1760.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- FastSpring and EBANX Forge Partnership to Expand Pix Payments for Digital Products in Brazil Apr 25, 2024

- Target Thursdays: NAS100, Robusta Coffee, USDCHF Apr 25, 2024

- QCOM wants to create competition in the AI chip market. Hong Kong index hits five-month high Apr 25, 2024

- Japanese yen hits all-time low as BoJ meeting commences Apr 25, 2024

- TSLA shares rose on a weak report. Inflationary pressures are easing in Australia Apr 24, 2024

- USDJPY: On intervention watch Apr 24, 2024

- Euro gains against the dollar amid mixed economic signals Apr 24, 2024

- PMI data is the focus of investors’ attention today. Turkey, Iraq, Qatar, and UAE signed a transportation agreement Apr 23, 2024

- Australian dollar rises on strong economic indicators Apr 23, 2024

- Geopolitical risks in the Middle East are declining. China kept interest rates at lows Apr 22, 2024