By Lukman Otunuga Research Analyst, ForexTime

It’s been a fairly quiet start to the week in many markets with FX ranges narrow and directionless trading in the dollar after the signature US payrolls data last week failed to embolden either the bulls or the bears. Asian markets are mixed and European bourses have opened up in similar fashion. That said, global equity indices are still sitting near to record / cycle highs as the Fed’s patient message continues to mean the stimulus punchbowl are still being passed around.

We had another reminder this morning about rising price pressures with China’s producer prices increasing at their fastest pace in 13 years. Soaring commodity prices as well as a low base effect after being in negative territory for most of last year has seen the index jump in recent months. This will add to global inflationary pressures and perhaps more action from the Chinese government economic planning agency who last month warned of “excessive speculation” in commodity markets and a crack down on monopolies.

Majors rangebound

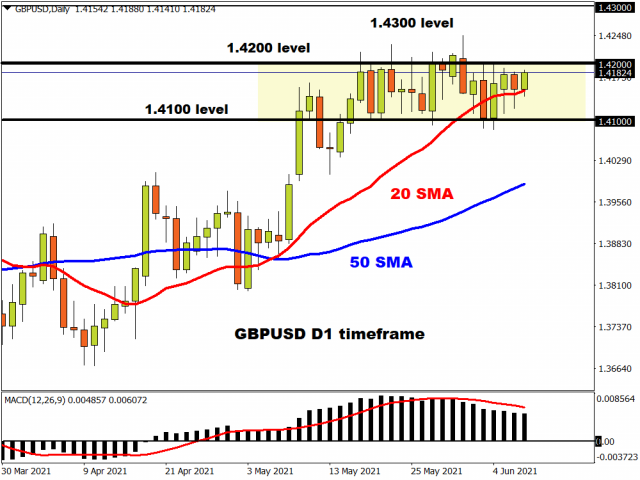

Expect more quiet trade in dollar crosses today ahead of the US CPI data and ECB meeting tomorrow. Sterling is trapped in a 1.41-1.42 range with the reopening delay not unduly worrying markets that much. June 21 has been in the minds of many in the UK, but a postponement of a couple of weeks is being signalled by the government.

Free Reports:

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

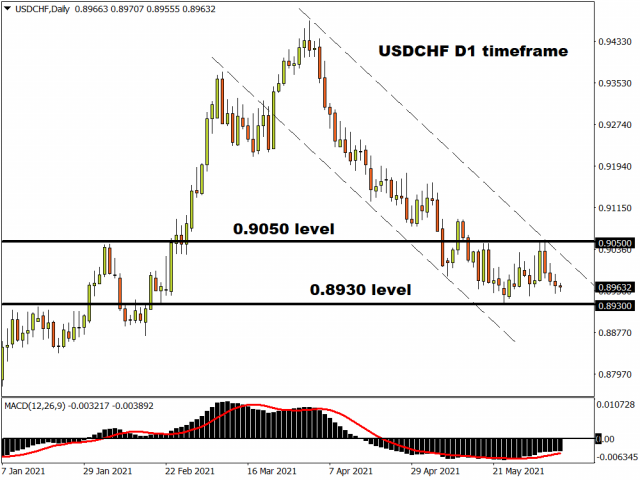

The swissie has been attracting buyers this week ahead of the ECB meeting tomorrow with USD/CHF back into its descending channel after venturing north last week above 0.9050. Bear will target the cycle low at 0.8930 unless the US inflation data prints to the topside of estimates.

Bank of Canada to stand pat

After shifting to a hawkish bias at its last meeting in April with the signalling of a rate rise in late 2022 and a second taper of its QE program, the leading hawkish central bank of the moment is set to wait for more post-lockdown data before continuing on its merry way to policy normalisation. A positive tone is expected from the Bank of Canada with an impressive vaccine rollout and strong CPI figures offset by two months of disappointing jobs data.

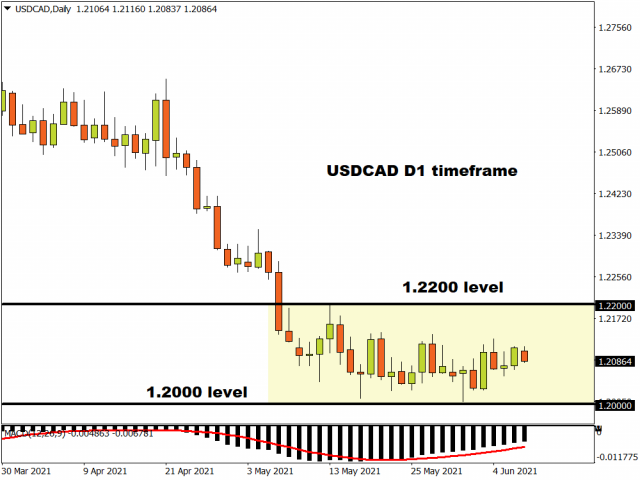

USD/CAD continues to consolidate above long-term support around 1.20. Any rebounds have been lacking in momentum with prices only moving above 1.22 on one occasion since mid-May. A downside break needs to develop sooner rather than later though as otherwise a deeper retracement may come into play.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- The US natural gas prices fell to a 2-month low. A drop in the technology sector on Wednesday had a negative impact on the broad market Apr 18, 2024

- Target Thursdays: Cocoa, Bitcoin and USDCHF hit targets! Apr 18, 2024

- British Pound shows signs of recovery amid favourable inflation data Apr 18, 2024

- Indices decline amid hawkish comments from the Fed. Investors are waiting for Israel’s answer Apr 17, 2024

- EURGBP: Slams into support on hot UK inflation Apr 17, 2024

- Brent crude prices dip amid concerns over global demand Apr 17, 2024

- Stock indices sell-off amid rising geopolitical tensions in the Middle East. China’s GDP grew the most in a year Apr 16, 2024

- New FXTM commodity hits all-time high! Apr 16, 2024

- NZD hits five-month low against strong US dollar Apr 16, 2024

- Escalating conflict in the Middle East is forcing investors to shift funds to safe assets Apr 15, 2024