By Lukman Otunuga, Research Analyst, ForexTime

A wave of risk aversion flooded U.S. markets on Monday as surging global coronavirus cases raised the prospects of fresh lockdown measures across the world.

Wall Sreet closed sharply lower as shares in more than 80% of the companies in the S&P 500 tumbled. The downside was further fuelled by growing caution ahead of the key U.S runoff elections in Georgia which will determine whether Democrats take effective control in Congress. With investors likely to adopt a guarded approach in the face of surging coronavirus cases and U.S. political uncertainty, equity markets may be exposed to downside losses.

Asian markets mostly fell on Tuesday morning amid the risk-off mode with the negative vibe likely to drag European shares lower. Given how global coronavirus infections have topped 85.6 million and a faster-spreading variant is triggering new lockdowns, things could get ugly.

England enters third lockdown…

At the start of the week, there were whispers around the UK imposing fresh draconian lockdown measures to limit the spread of the new COVID-19 variant.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

Download Our Metatrader 4 Indicators – Put Our Free MetaTrader 4 Custom Indicators on your charts when you join our Weekly Newsletter

This became a reality yesterday evening after Boris Johnson announced that everyone in England must stay at home except for legal reasons.

The fresh lockdowns may raise fears around the UK economy facing a deeper double-dip recession while fuelling speculation around a potential interest rate cut by the Bank of England.

This sentiment is being reflected in the British Pound which has weakened against almost every single G10 currency excluding the Dollar since Monday.

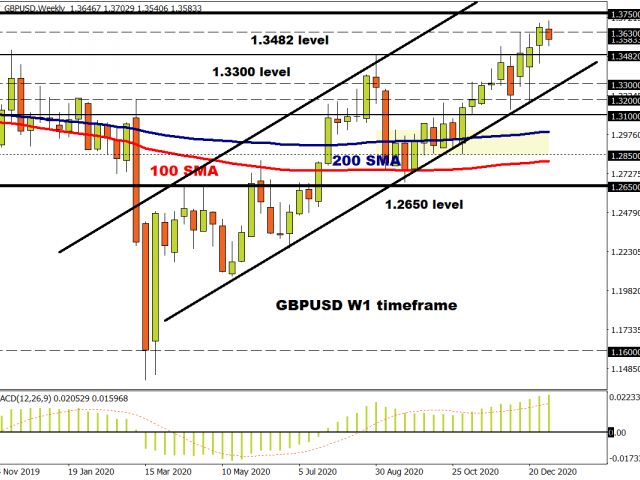

Looking at the technical picture, the road ahead for Sterling for filled with many obstacles and potholes. Although the UK and EU were able to secure a Brexit deal before the transition deadline, many questions remain unanswered. The swelling coronavirus cases and lockdowns have added another element of uncertainty to the Pound’s depressing outlook.

Focusing on the GBPUSD, sustained weakness below 1.3630 could open the doors towards 1.3482 and 1.3400 respectively. If bulls can break back above 1.3630, the next key point of interest may be found around 1.3750.

OPEC+ extends talks to second day

Anyone surprised that OPEC+ talks were unexpectedly suspended thanks to disagreements over whether to raise output in February?

Yesterday, we highlighted that the talks could be complicated due to Russia’s insistence to release more barrels into the markets. Expect Oil prices to edge lower amid the ongoing uncertainty until a decision is made. If OPEC+ decides to leave production unchanged at current levels, this could provide a welcome boost to Oil prices.

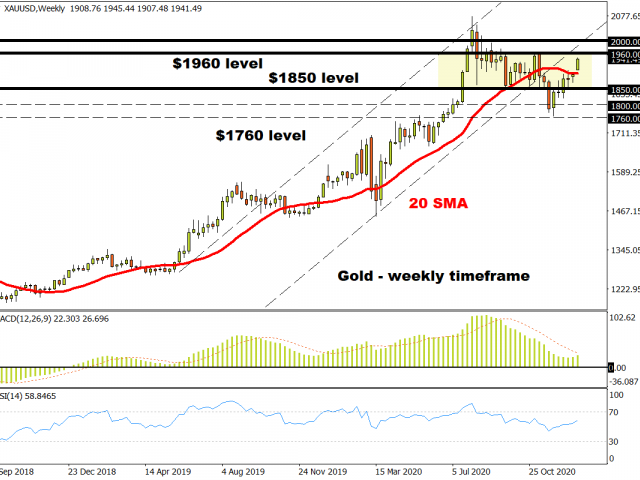

Commodity spotlight – Gold

Gold continues to derive strength from a broadly weaker Dollar, surging coronavirus cases, and expectations over looser monetary policy in the face of tougher lockdowns.

Prices have the potential to challenge $1960 in the near term and possibly $2000 over the next few weeks if the current themes weakening the Dollar remain intact. Talking technicals, the precious metal is respecting a bullish trend with the daily close above $1930 encouraging a move towards $1960.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- COT Metals Charts: Speculator bets led by Copper & Silver Apr 20, 2024

- COT Bonds Charts: Speculator bets led by 10-Year Bonds & Fed Funds Apr 20, 2024

- COT Stock Market Charts: Speculator bets led by S&P500-Mini Apr 20, 2024

- COT Soft Commodities Charts: Speculator bets led by Soybean Meal & Lean Hogs Apr 20, 2024

- 3 Signs of Developing U.S. Economic Slowdown Apr 19, 2024

- Israel has retaliated against Iran. Investors run to safe assets Apr 19, 2024

- Gold hits record high amid growing geopolitical tensions Apr 19, 2024

- The US natural gas prices fell to a 2-month low. A drop in the technology sector on Wednesday had a negative impact on the broad market Apr 18, 2024

- Target Thursdays: Cocoa, Bitcoin and USDCHF hit targets! Apr 18, 2024

- British Pound shows signs of recovery amid favourable inflation data Apr 18, 2024