By Han Tan, Market Analyst, ForexTime

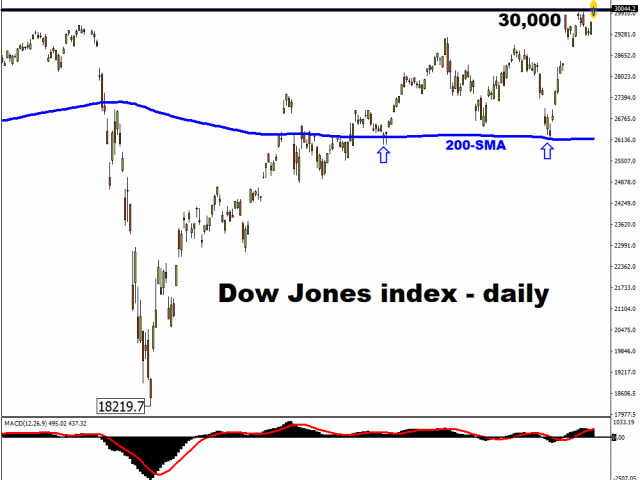

Last week, I wrote about how a Dow Jones index that reads above 30,000 was a matter of when, not if.

That day has now arrived.

The Dow posted a closing price above the 30,000 mark for the first time in its history on Tuesday. And with stock futures pointing north at the time of writing, there could be more gains to be had in Wednesday’s session, before US markets close for Thanksgiving on Thursday.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

The gains in US equities were powered by stocks in the energy and financial sectors, as investors stuck to the US economic reopening theme, prompting the S&P 500 to also post a new record high.

Risk assets have clearly been heartened by positive developments on key fronts: a surer transition for the US Presidency, a dovish US Treasury Secretary waiting in the wings, and a third Covid-19 vaccine supplier that’s closer to rollout.

Such headlines have only emboldened traders to flock to the markets, bucking the sleepy trend that’s typically associated with this time of the year. US exchanges have seen 13 billion shares being traded per day so far this week, which is a whopping 75 percent more volume compared to the same period in 2019! Looks like the shopping spree isn’t limited to Christmas stocking stuffers this year.

As long as the narrative surrounding the vaccine-enabled global economic recovery isn’t derailed, along with the Fed’s ultra-accommodative stance staying intact, that ensures that this rally has more room to run going into 2021. The FXTM Trader’s Sentiments are net long on the US SPX 500 (Mini).

Dollar in the doldrums?

The Dollar index (DXY) will also be in focus today, amid a slew of US economic data. Before investors can dig into servings of freshly-carved Turkey meat and stuffing, they must first digest the latest US weekly jobless claims, October personal spending, and the second reading of Q3 GDP, all to be released on Thanksgiving-eve. Further signs of an economic recovery that could meaningfully boost US inflationary pressures could send the DXY below the psychologically-important 92.0 level, with the September low of 91.74 next in its sights.

Then there’s the latest FOMC meeting minutes as well, also due on Wednesday. Investors will be eyeing how the Fed intends to boost its support measures for the world’s largest economy, with such a decision potentially arriving at the central bank’s meeting in December. Should investors get a stronger whiff of more incoming stimulus, that could fuel more gains for riskier assets while prompting safe haven assets such as the US Dollar to explore more of its downside.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- TSLA shares rose on a weak report. Inflationary pressures are easing in Australia Apr 24, 2024

- USDJPY: On intervention watch Apr 24, 2024

- Euro gains against the dollar amid mixed economic signals Apr 24, 2024

- PMI data is the focus of investors’ attention today. Turkey, Iraq, Qatar, and UAE signed a transportation agreement Apr 23, 2024

- Australian dollar rises on strong economic indicators Apr 23, 2024

- Geopolitical risks in the Middle East are declining. China kept interest rates at lows Apr 22, 2024

- Brent crude dips to four-week low amid easing geopolitical tensions Apr 22, 2024

- COT Metals Charts: Speculator bets led by Copper & Silver Apr 20, 2024

- COT Bonds Charts: Speculator bets led by 10-Year Bonds & Fed Funds Apr 20, 2024

- COT Stock Market Charts: Speculator bets led by S&P500-Mini Apr 20, 2024