By Han Tan, Market Analyst, ForexTime

A week is a long time…in markets!

It’s been a volatile few sessions for risk assets with disappointing results from the Tech titans adding to the fickle and rather febrile sentiment currently swirling around. Perhaps that’s to be expected with investors now focused more on what could go wrong as election week approaches. Markets have been playing the post-election reflation trade for the global economy into 2021, but there is certainly room for disappointment and especially if it takes a lot longer to figure out the eventual occupant of the Oval Office for the next four years.

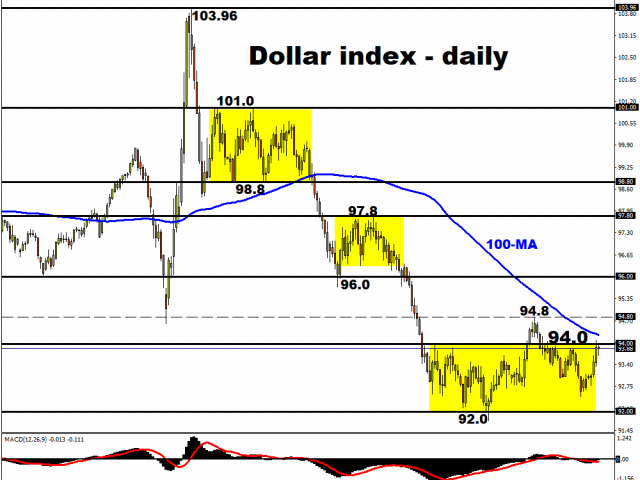

King Dollar is mixed on the day and checked by the 94 mark, but the greenback is on track for its strongest weekly performance in five amid the heightened risk aversion. It seems there is now a lot more talk of a closer US election than previously thought, with some of the key swing states like Pennsylvania, Michigan and Wisconsin unable to start counting early votes until Tuesday, meaning it is highly unlikely they will able to make a final announcement on election night.

The gloomy mood has been exacerbated by last night’s Big Tech earnings which beat analyst expectations, but disappointed on various other issues. For example, Apple and Facebook are both down around five percent, the former reflecting disappointment that the company did not release holiday quarter revenue guidance, while Facebook is still scolded by the bruising hearing from both Republicans and Democrats this week.

Free Reports:

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Get our Weekly Commitment of Traders Reports - See where the biggest traders (Hedge Funds and Commercial Hedgers) are positioned in the futures markets on a weekly basis.

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

Sign Up for Our Stock Market Newsletter – Get updated on News, Charts & Rankings of Public Companies when you join our Stocks Newsletter

No support from record Eurozone GDP

The deteriorating situation in Europe concerning the rising infection and hospitalisation rates has overshadowed the (mixed) data released this morning. The region’s economy expanded by 12.7 percent in the third quarter after an 11.8 percent contraction in the previous quarter. But the record rebound still leaves Eurozone growth over four percent below its late-2019 high. A drop in the final quarter of this wretched year is now likely, which of course is prompting the ECB to pre-commit to extra stimulus measures in December. Will a determined Lagarde be pushed into action sooner?

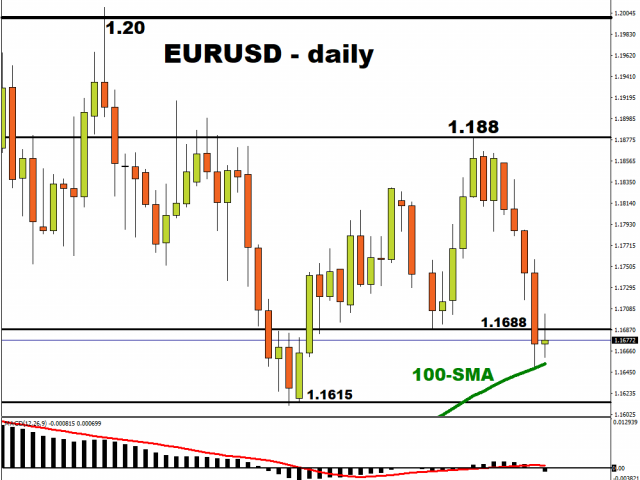

The 100-day moving average in EURUSD is acting as support at the moment with the world’s most heavily traded currency pair bouncing off yesterday’s low. The weekly close will be important to see if prices can hold below 1.1688 and break previous weekly support over the last few weeks. There looks like little support until 1.1615 after this.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

![]() Article by ForexTime

Article by ForexTime

ForexTime Ltd (FXTM) is an award winning international online forex broker regulated by CySEC 185/12 www.forextime.com

- 3 Signs of Developing U.S. Economic Slowdown Apr 19, 2024

- Israel has retaliated against Iran. Investors run to safe assets Apr 19, 2024

- Gold hits record high amid growing geopolitical tensions Apr 19, 2024

- The US natural gas prices fell to a 2-month low. A drop in the technology sector on Wednesday had a negative impact on the broad market Apr 18, 2024

- Target Thursdays: Cocoa, Bitcoin and USDCHF hit targets! Apr 18, 2024

- British Pound shows signs of recovery amid favourable inflation data Apr 18, 2024

- Indices decline amid hawkish comments from the Fed. Investors are waiting for Israel’s answer Apr 17, 2024

- EURGBP: Slams into support on hot UK inflation Apr 17, 2024

- Brent crude prices dip amid concerns over global demand Apr 17, 2024

- Stock indices sell-off amid rising geopolitical tensions in the Middle East. China’s GDP grew the most in a year Apr 16, 2024